Diana Mejía

María Saavedra

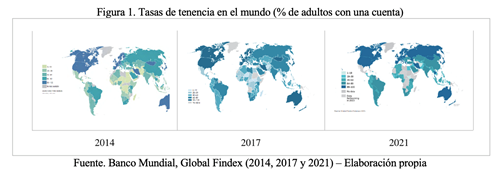

Recent results from the World Bank’s Global Findex 2021 show a widespread surge in account holdings at financial institutions around the world. In 2011, the percentage of adults worldwide who held an account was at 51%, and three years later, it stood at 62%, then at 69% in 2017, finally reaching 76% in 2021. As Figure 1 shows, in countries such as Canada and the United States, between 90% and 100% of the adult population, on average, holds at least one individual or joint account since 2011. Meanwhile, in Latin America, countries such as Colombia, Peru and Bolivia have experienced an increase in the average number of adults who have held an account since 2014. Thus, the increase has been 20 percentage points in Colombia, 30 points in Peru and 27 points in Bolivia.

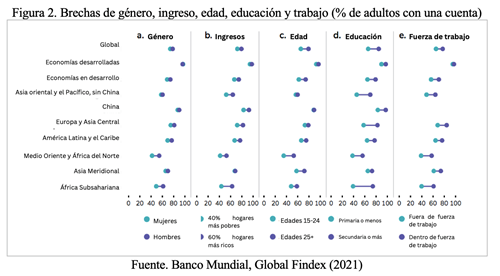

However, when examining the differences by gender, income, education level and labor market share for 2021, gaps persist in all regions of the world, although more exacerbated in some regions than in others. Specifically, in Latin America and the Caribbean (LAC), education and labor market share gaps are the highest, while in developed economies, gaps are almost non-existent between women and men, between the poorest and richest households, and between those in (employed) and out (unemployed or seeking employment) of the labor force (Figure 2).

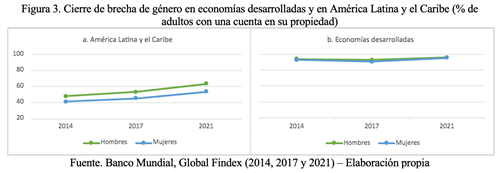

According to the latest Global Findex report, the gender gap has gradually closed globally since 2014. Developed economies, for example, experienced a closing gap of around 2 percentage points over the years (Figure 3). However, this trend is not observed in LAC, where the report shows that, while overall account holding increased, the gender gap widened by approximately 3 percentage points. According to studies conducted at CAF based on the results of financial capacity surveys in several countries of the region, gender gaps are evident not only in the access and use of financial products, but also in financial knowledge, skills, attitudes, and behaviors, resulting in lower levels of financial well-being for women.

Between 2014 and 2021, the proportion of adults who made digital payments doubled from 26% to 51% worldwide. For LAC, this figure went from 5% in 2014 to 20% in 2021, i.e. a 15-percent increase. When analyzing the gender gap in payments through a mobile money account, we find that in LAC men are, on average, 11 percentage points more likely to use this type of digital payments than women, while in developed economies the difference is only 4 percentage points.

The increase in account holding in LAC is mainly due to increased access to mobile money accounts from government subsidy payments in response to the crisis resulting from the Covid-19 pandemic, which has allowed a higher proportion of women, low-income groups and other sectors traditionally excluded from the financial system can access financial products.

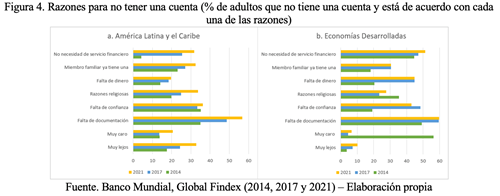

Although the proportion of people who do not have an account has been decreasing since 2014 in LAC, 41.67% of adults in the region still lack access to an account according to Global Findex figures for 2021. The main reason people argue for not holding an account in LAC is lack of documentation, followed by lack of trust in financial institutions (Figure 4).

Regarding use, of the total number of people who claim to have an account, some did not make any deposits or withdrawals in the last year. In LAC, there is evidence of a 10 percentage point increase in inactive accounts from 2014 to 2021, while in developed economies this increase was significantly lower, of 0.7 percentage points.

In the 2021 Global Findex, questions were added to understand the reasons why people keep inactive accounts and fail to make any deposits or withdrawals. When analyzing the results, we found that the three main reasons for inactive accounts are similar to those expressed for not having an account: i) the remoteness of the branches of the financial institution, ii) the lack of confidence in the system, and iii) the conviction of not needing one. Faced with the second reason, it is important that financial literacy strategies include programs to improve consumer confidence in digital financial services. Similarly, it is essential to strengthen financial consumer protection schemes and cybersecurity as well as information security policies.

On the other hand, the 2021 Global Findex includes questions aimed at measuring the financial well-being of the population, understood as the ultimate goal of financial inclusion or as the extent to which an individual or family can smoothly manage their current financial obligations and feel confident about their financial future. To analyze this variable, the 2021 Global Findex included questions related to financial resilience, financial stress, as well as confidence and independence to use financial products.

In order to obtain information on financial resilience, the Global Findex specifically asks questions about the difficulty of acquiring emergency funds in the 30 days following the survey. In LAC, only 20% of the population was able to obtain that amount, while in developed economies the percentage of adults who could do so is about 60%. Of this percentage, women are shown to be less resilient than men in both groups: The gap is 30 percentage points in LAC and only 5 percentage points in high-income developed economies.

Financial stress, conversely, refers to the financial concern of consumers. The survey included concerns about old age, medical costs, debt and education. The results show that, in both the region’s and developed economies, most adults worry about their finances. In fact, the biggest concerns were old-age costs (21% for LAC and 36% for developed economies) and medical costs (43% for LAC and 34% for developed economies), followed by debts (19% for LAC and 21% for developed economies) and education (15% for LAC and 7% for developed economies).

Lastly, the ability of adults to use financial products without assistance is greater in LAC economies than in developed economies. Specifically, 65% of adults in LAC use their account without any assistance, compared to 52% of adults in developed economies. This can be explained by the high proportion of seniors in developed economies, who, although are financially included, do not possess the digital literacy to use digital financial services and require help from a third party. Based on this result, noteworthy is the need to provide financial and digital literacy to the elderly: training tailored especially to them and that helps them understand and operate in the financial system adequately with the right skills.

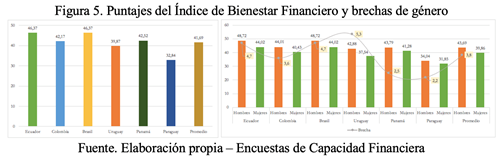

CAF has been measuring financial well-being in different countries of the region (Brazil, Colombia, Ecuador, Panama, Paraguay and Uruguay). When comparing the financial well-being index (score of 0 to 100) we found that it stands at 41.69 points on average (with Brazil and Ecuador scoring highest at 46.37 and Paraguay with the lowest score with 32.84 points) and gender gaps are observed in all countries (Figure 5).

In sum, the most recent results of the Global Findex for LAC show that, while there has been an increase in account holding in financial institutions, largely explained by the greater access to mobile money accounts as a result of the Covid-19 pandemic, its use still lags far behind that of developed economies. Additionally, gaps in gender, income, educational attainment and labor participation remain and, in some cases, have actually widened. These results show that, although access to accounts is a prerequisite for financial inclusion, it is not sufficient on its own, since there are barriers that prevent people from making effective use of the financial products to which they have access.

This implies that financial institutions should focus on designing financial products, as well as financial literacy programs, that are tailored to the needs of segments of the population excluded from the financial system (women, people with low incomes and educational attainment, unemployed, informal population, rural population, among others) which would yield significant improvements in their financial well-being.